Chapter 6 and Chapter 10 are both related to inventory management and moving chapter 10 to chapter 7 makes the flow much better. OpenStax does a good job of working an editorial process that eliminates any culturally insensitive content. On the recommendation of the American Institute of CPAs (AICPA), the FASB was formed as an independent board in 1973 to take over GAAP determinations and updates.

- GAAP is meant to ensure consistency, accuracy, and transparency in financial reporting and aims to provide a reliable foundation for investors to make informed decisions.

- At no point can a company or financial team choose to ignore or modify any of the regulations.

- In that case, the company might need to start considering the liquidation value of assets.

- I gave the text 3/5 as being both accessible prose and inaccessible (confusing) prose, adequate content and inadequate content.

- Reports must therefore be thorough and clear, without any omissions or modifications.

Compliance With GAAP

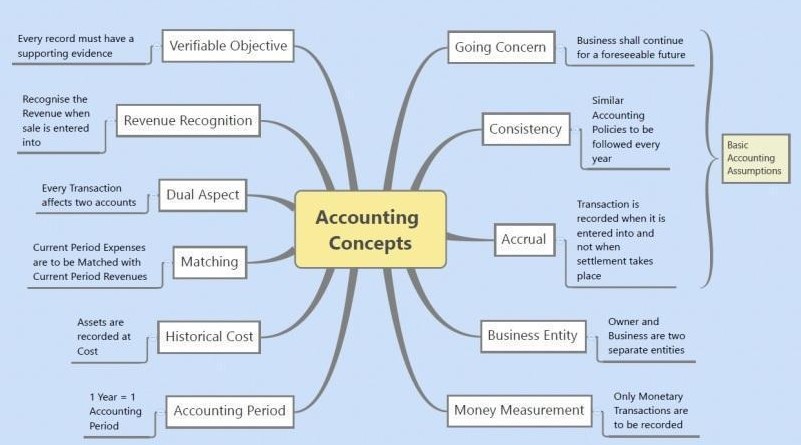

While SFRS is primarily based on International Financial Reporting Standards (IFRS), it incorporates certain adjustments to align with local laws and regulations. For example, if a company purchases inventory from a supplier, the transaction should be supported by a purchase order, invoice, and delivery receipt. These objective pieces of evidence validate the occurrence of the transaction and the amount recorded in the financial statements. In that case, the Principle of Prudence requires that an estimated loss be recorded in the financial statements. The accounting guideline that permits the violation of another accounting guideline if the amount is insignificant.

Understanding GAAP

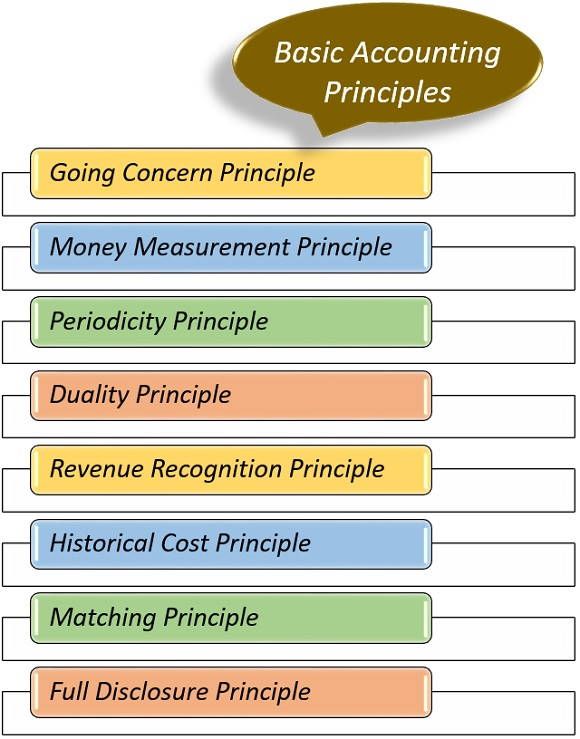

For instance, large companies usually have a policy of immediately expensing the cost of inexpensive equipment instead of depreciating it over its useful life of perhaps 5 years. When a cause-and-effect relationship isn’t clear, expenses are reported in the accounting period when the cost is used up. For example, the $120,000 cost of equipment with a 10-year life will be charged to expense at a rate of $1,000 per month.

Applications in Financial Analysis

Any financial statement must accurately reflect all of the company’s assets, expenses, liabilities and other financial commitments. Reports must therefore be thorough and clear, without any omissions or modifications. All negative and positive values on a financial statement, regardless of how they reflect upon the company, must be clearly reported by the accounting team. Accountants cannot try to make things look better by compensating a debt with an asset or an expense with revenue.

Create a Free Account and Ask Any Financial Question

It would be fairly easy to divide the content, it would just take a little more work to find the right page. I appreciate the efforts the authors put into the creation of this book. I especially applaude the ethical discussions and “uses of technology” in the chapters. Our mission is to empower readers with the most factual and reliable financial information possible to help them make informed decisions for their individual needs.

What is an example of GAAP?

This book is widely recognized as an authoritative source for accounting practices. It provides detailed explanations of GAAP principles and their applications in various scenarios. GAAP principles are integral to maintaining the integrity and reliability of financial reporting. Comprehending these principles is vital to guaranteeing openness and uniformity in financial documentation, 5 principles of accounting essential for efficient financial markets and the economy. Each quarterly report provides a snapshot of the company’s performance and financial position, which is crucial for short-term analysis and decision-making. For example, consider a retail company that reports its revenues, expenses, profits, and other financial metrics at the end of each quarter of a year.

In this fact—namely, acceptance by all concerned—lies the importance of adhering to these accounting concepts or assumptions. Everyone accepts this assumption and all accounting records and statements prepared on the basis of this assumption are generally accepted by all concerned. The GAAP has gradually evolved, based on established concepts and standards, as well as on best practices that have come to be commonly accepted across different industries. In addition, or as an alternative, are the International Financial Reporting Standards (IFRS) established by the International Accounting Standards Board (IASB). The IFRS rules govern accounting standards in the European Union, as well as in a number of countries in South America and Asia. Standard costing has been a foundational tool in cost accounting for decades, helping businesses set predetermined costs for products and measure variances against actual costs.

I’ve used two textbooks for my course in the last five years and the information is comparable. There is much consistency between the chapters in terms of how they are structured. The life examples are drawn from companies which are relevant and understandable to students today.

This principle is critical in ensuring that financial statements provide a realistic and not overly optimistic view of a company’s financial status. The essence of this principle lies in its demand for uniformity in the application of accounting techniques across different reporting periods. It prevents arbitrary changes in accounting methods that could distort a company’s financial performance and position. The Principle of Sincerity is a fundamental ethic in accounting under the umbrella of Generally Accepted Accounting Principles (GAAP). It underscores the need for accuracy and impartiality in financial reporting. The principle is not merely a technical requirement but a moral imperative that guides accountants and financial professionals in their work.

Any red flags in the company’s finances get identified, making it easy to compare the details over a specific period. I thought the problems and examples were very well done but I did have a problem with the pacing of the material especially in the first few chapters. If these were early level accounting students I think they would have been lost in the first 3 chapters due to the complexity of the concepts introduced early in the text. In general, the book provides coverage in appropriate depth to support the needs of a first year accounting curriculum. In reviewing some of the aspects within the internal control chapter, for instance, there is appropriate emphasis on the Foreign Corrupt Practices Act as well as the Sarbanes-Oxley Act.

Leave a Reply